We have witnessed multiple transformation phases on this island. We have moved far beyond the era of sprawling, multi-hectare estates. Today, in the first quarter of 2026, spatial efficiency and data metrics dictate the market.

If you are planning to park your capital in Bali’s property sector this year, discard the outdated narratives about finding a “hidden paradise.” Let’s look at the hard numbers, market competition, and risk mitigation strategies based on the latest Q1 2026 market reports from REID and Colliers.

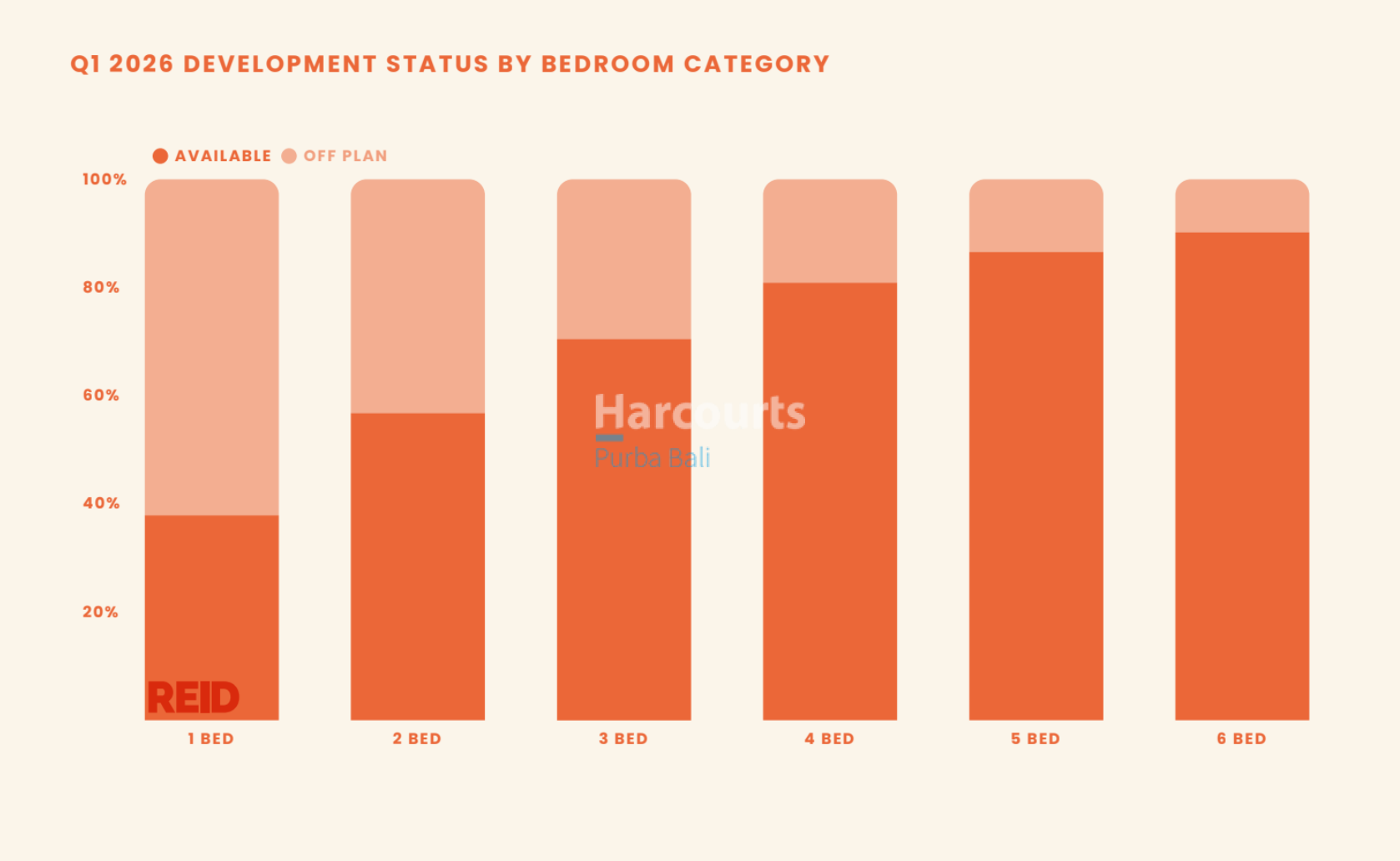

The Asset Profile Shift: Compact is King

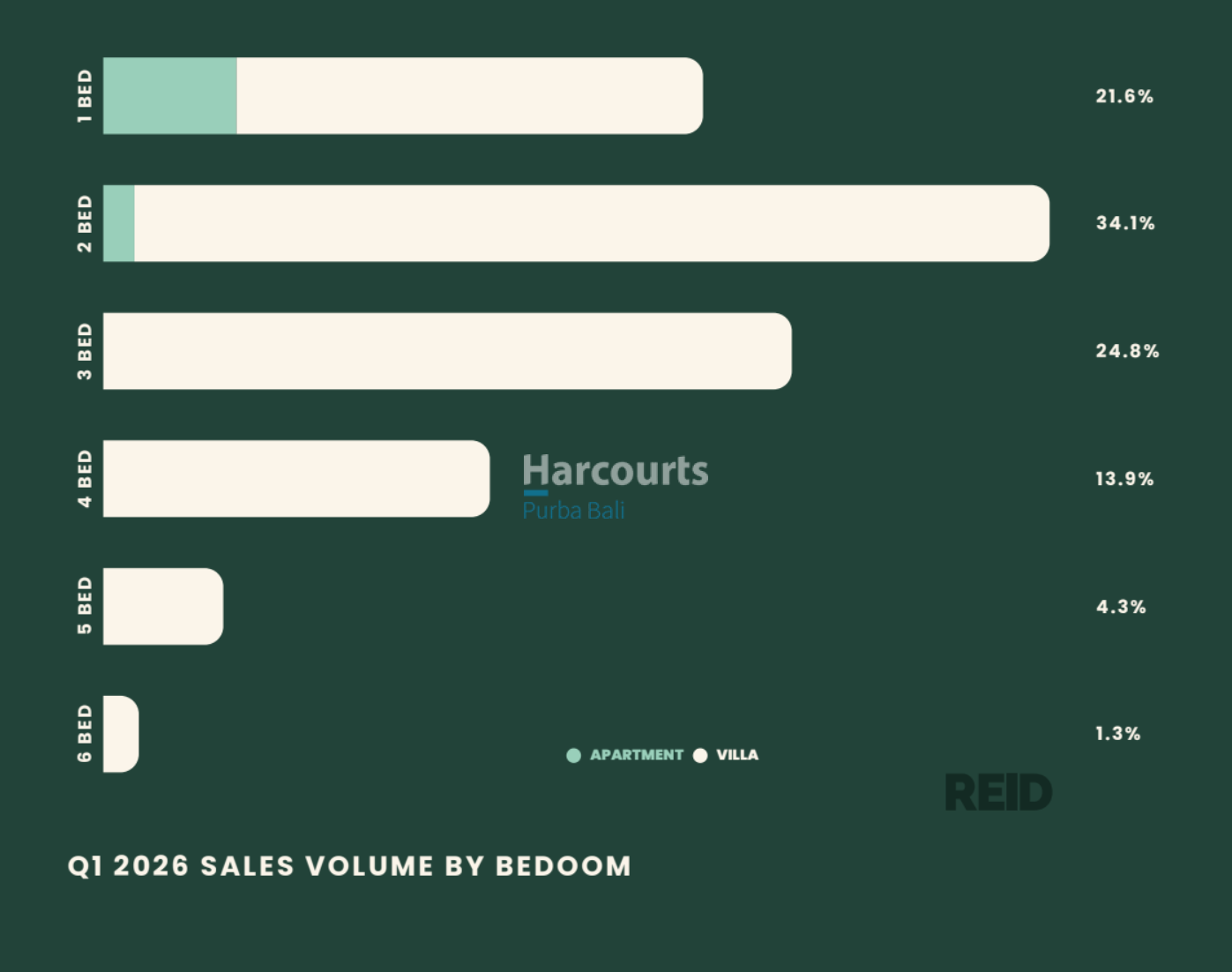

The Bali property market is currently undergoing a highly rational consolidation phase. Based on this quarter’s transaction data, over 55% of the sales volume is captured by compact assets—specifically 1-bedroom and 2-bedroom properties.

To give you exact dimensions, the market average for a 1-bedroom villa currently sits at 65 square meters, while a 2-bedroom unit averages 140 square meters. Why is this structural shift happening?

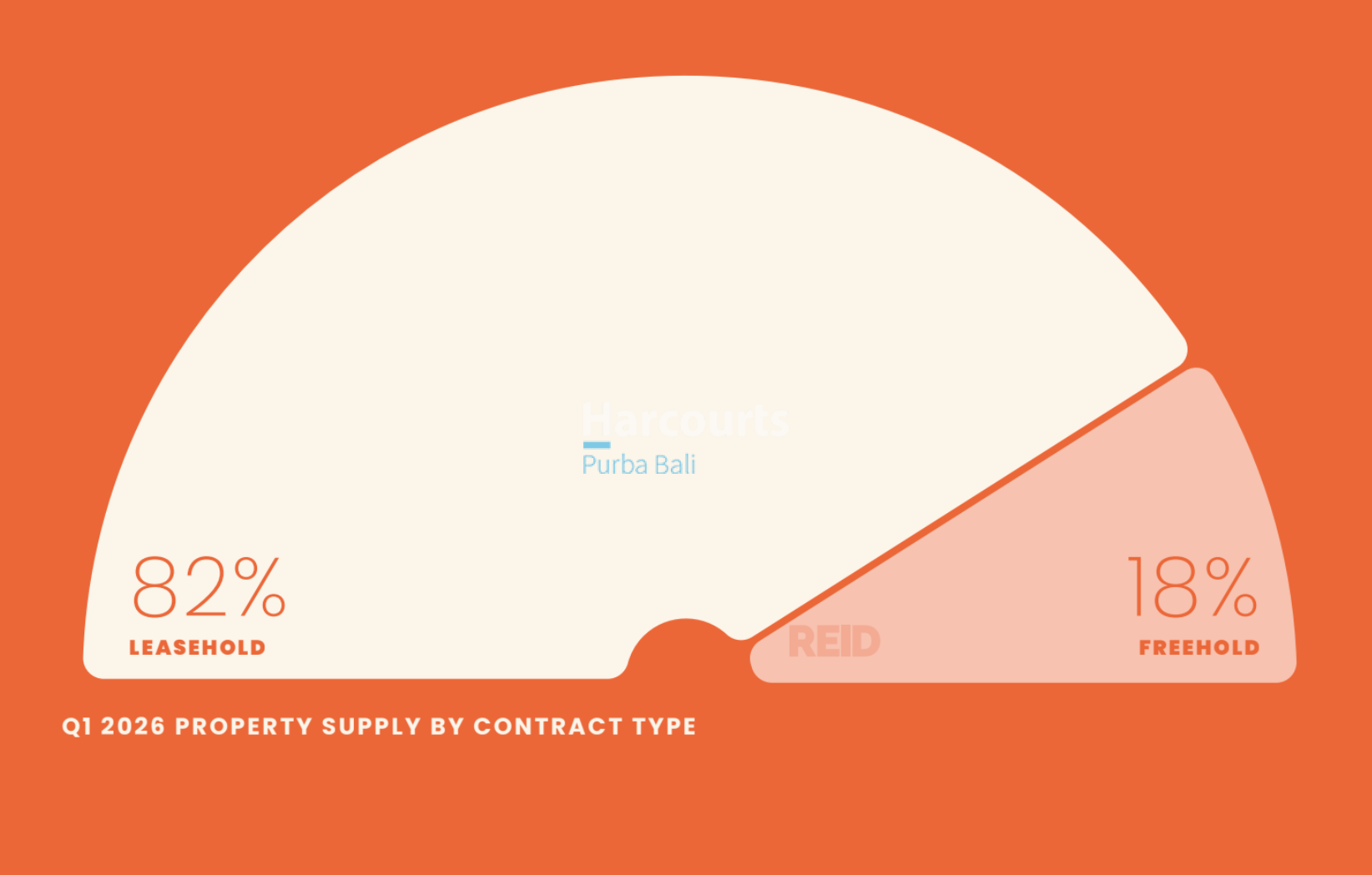

The answer lies in shifting tourism demographics. Generation Z and independent travelers now drive arrival numbers. They are not looking for vast land sizes; they prioritize spatial efficiency, smart home connectivity, and sustainable building designs featuring cross-ventilation and vertical gardens. This reality pushes investors to build smaller footprints with much faster daily rental turnovers. Consequently, current property supply relies heavily on the villa segment (87%), with the vast majority structured under Leasehold legal titles (82%).

Independent Villas Eating Hotel Market Share

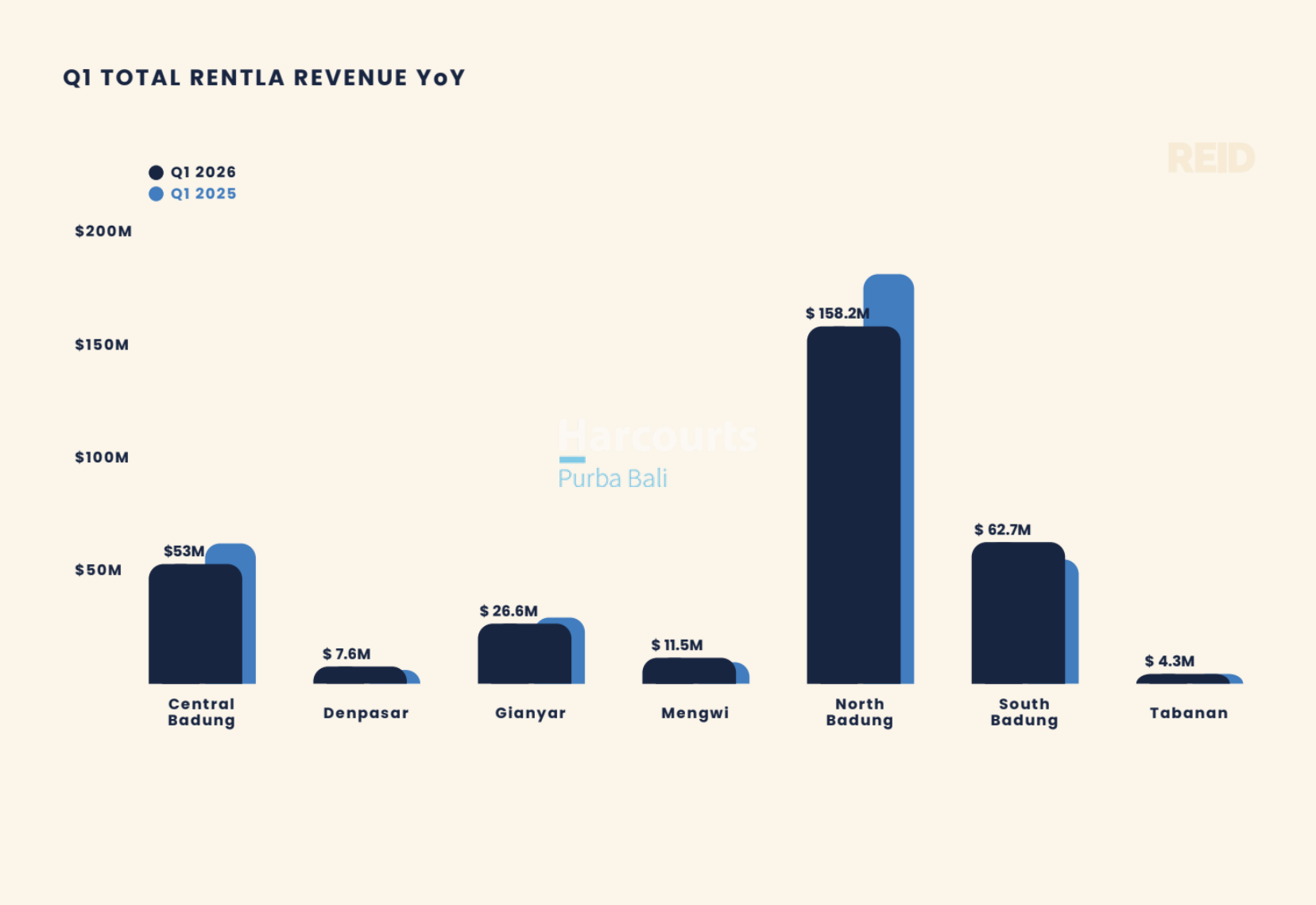

The latest hospitality sector reports reveal a compelling metric: 5-star hotel occupancy in premium areas is facing direct pressure from independent villas.

These independent properties are no longer amateur setups; they utilize commercial-grade building materials, feature technical specifications on par with starred hotels, and employ professional property management frameworks.

With foreign tourist arrivals hitting 42% of total visitors (the highest since 2019), these independently managed villas successfully capture market segments that traditionally booked large hotels in Nusa Dua or Seminyak. The impact? We are seeing a 3.4% Year-on-Year (YoY) increase in villa rental occupancy, proving that demand for private, well-specified assets continues to absorb market supply.

Completed vs. Off-Plan: Buying Time with a 20% Premium

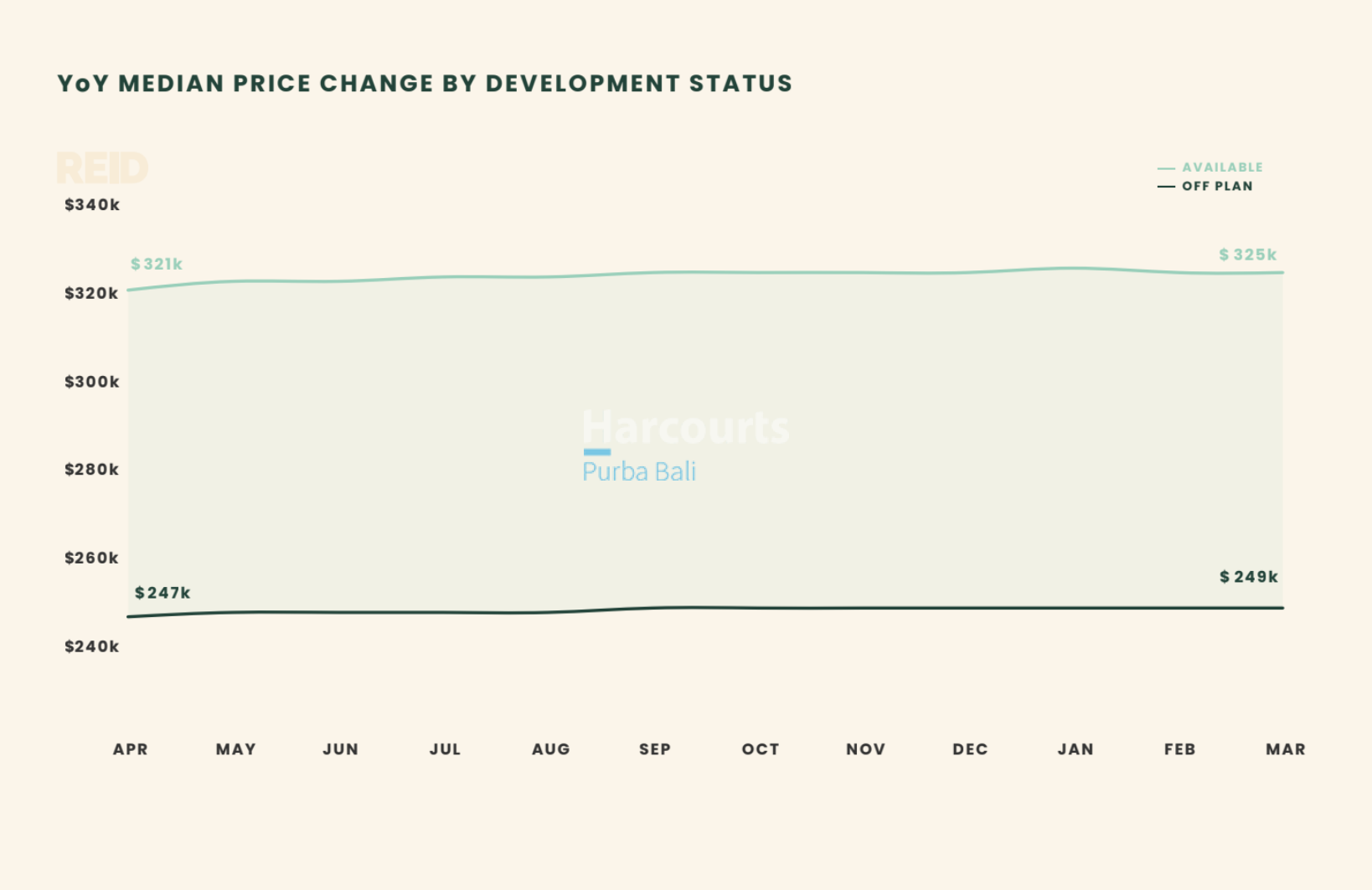

One of the most crucial metrics for our clients at Harcourts Purba Bali right now is the pricing gap between off-plan projects and completed, available builds.

The data highlights a price difference of up to 20% between the two. Today’s buyers are consciously willing to pay an approximate 15% premium for fully operational villas. This is a highly calculative move: given the volatility of raw material costs and construction timeline risks, purchasing a completed villa measuring 205 square meters (the current overall market average) means you immediately cut out the waiting period and begin generating rental yield in the first month of handover.

In premium corridors like Central Badung and South Badung, this strategy of acquiring completed assets is proven to shield investors from construction price fluctuations while allowing them to capitalize on current quarter momentum.

Conclusion for Your 2026 Strategy

The Bali market in 2026 is no longer speculative; it is a market driven by operational yield and spatial efficiency. Allocating your capital into 1 or 2-bedroom properties with clear building specifications, measurable locations, and structured Leasehold titles is the most secure strategy based on current data metrics.

Want to dissect this data further for your portfolio? Our team at Harcourts Purba Bali has direct access to property inventory that precisely matches the analytical criteria above. Contact us for data-driven consultation, not just marketing narratives.